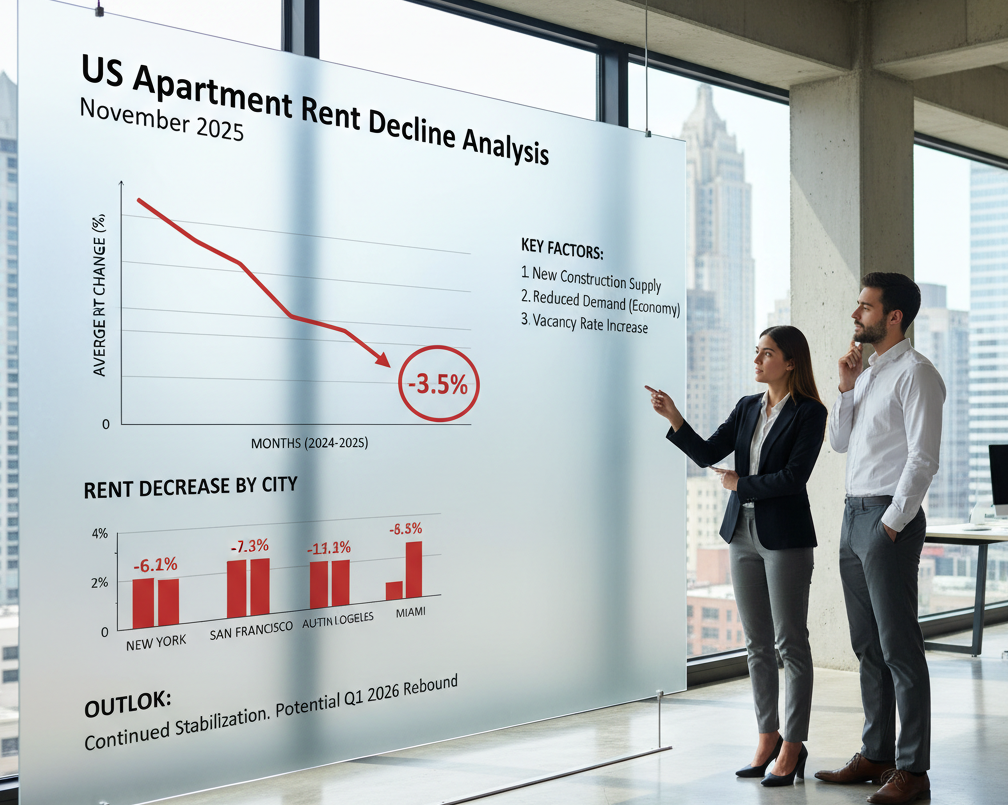

US Apartment Rent Decline Analysis: November 2025

The State of the Rental Market

Rents across the United States are officially on the decline — and at a pace not seen in over 15 years.

As of November 11, 2025, the national average rent dropped to $1,708 in October, a 0.3% month-over-month decrease from September’s $1,713. That might not sound like much, but it marks the steepest October drop in more than a decade and a half, and the fourth straight month of stagnant or negative rent growth.

Year-over-year, rent growth has nearly stalled — now sitting at just 0.8%, down sharply from 1.5% at the start of 2025. In fact, three of the five largest monthly rent declines in the last 15 years have occurred within just the past three months.

Where Are Rents Falling the Most?

🏜️ Sun Belt & Mountain West Hit Hardest

Markets that saw massive apartment construction booms are now facing oversupply and steep rent corrections.

Biggest Monthly Rent Drops (October 2025):

- Denver: -1.3% month-over-month, -3.7% year-over-year

- Austin: -1.1% month-over-month, -4.6% year-over-year

- Seattle: -0.9% month-over-month

- Salt Lake City: -0.8% month-over-month

- Phoenix: -0.8% month-over-month

Florida Gulf Coast Struggles Continue:

- Cape Coral: -9.9% year-over-year

- Sarasota: -5.6%

- Fort Myers: -4.4%

- Naples: -3.8%

- Miami: -6.0% year-over-year (though stabilizing month-over-month)

🌆 Cities That Are Holding Strong

While much of the Sun Belt and Mountain West see declines, some supply-constrained metros are bucking the trend:

- San Francisco: +5.8% year-over-year

- San Jose: +3.8%

- Chicago: +3.6% (+4.3% on some platforms)

- Norfolk: +3.0%

- New York: +2.5%

All four US regions reported monthly rent declines in October — with the West (-0.53%) and South (-0.28%) hit hardest, while the Midwest (-0.18%) remains the most stable.

What’s Driving the Rent Decline?

1️⃣ Oversupply of New Apartments

The number one factor is simple: too much new construction.

Over 560,000 new apartment units have been added nationwide in the last 12 months — most of them in high-growth metro areas. Another 920,000 multifamily homes remain under construction, more than 50% higher than pre-pandemic levels.

Vacancy rates in large buildings hit 8.2% in early 2025, the highest in four years. Sun Belt cities like Austin, Phoenix, and parts of Florida built aggressively during the pandemic, and are now facing the consequences — higher vacancies and declining rents.

2️⃣ Economic and Labor Market Pressures

Job growth has slowed, especially in tech-heavy regions like Seattle, where layoffs at major employers (including Amazon) have softened demand. Meanwhile, median household incomes have grown about 2.8%, outpacing rent increases — a rare win for affordability.

3️⃣ Mortgage Barriers Keeping Renters in Place

Despite falling rents, high mortgage rates continue to keep many renters from buying homes.

With average 30-year mortgage rates hovering around 6.35–6.9%, and only 12% of households able to afford the median-priced home, the rental market still enjoys underlying demand even as prices cool.

4️⃣ The Fed’s Interest Rate Shifts

After months of elevated rates, the Federal Reserve began cutting rates in late 2025 — a move expected to gradually stabilize the market. Construction financing had become expensive, slowing new project starts, which may relieve future oversupply pressures.

What’s Next for 2026?

Experts predict that rents may bottom out by early 2026, with gradual stabilization and 2–3% national rent growth expected later in the year.

Why the Outlook Is Improving:

- New apartment construction has dropped sharply — starts are down over 70% from 2022 peaks.

- Demand is rebounding — Q4 2025 could mark the first time since 2021 where more units are being leased than built.

- Forecasts from CoStar and RealPage suggest rent growth will resume modestly by mid-2026.

However, markets like Austin, Denver, and Florida’s Gulf Coast will likely take longer to recover due to lingering oversupply. In contrast, coastal cities like San Francisco, New York, and Boston — with limited buildable land — are already seeing rent rebounds.

Takeaway

- National average rent (Oct 2025): $1,708

- Annual rent growth: +0.8% (down from +1.5% in January)

- Main driver: Oversupply of 900,000+ units in high-growth metros

- Forecast: Stabilization by late 2025; moderate 2–3% rent growth in 2026

For renters, now is a prime opportunity to negotiate better deals or upgrade apartments before the next cycle of increases.

For landlords, 2026 may represent the start of a more balanced, sustainable rental market after two years of supply shocks.

🧾 Disclaimer

The information provided in this article is based on publicly available research and data from reputable real estate and financial sources as of November 2025.

While every effort has been made to ensure accuracy, readers are encouraged to conduct their own research or consult with qualified professionals before making housing or investment decisions.

We hold no responsibility for any inaccuracies or changes in market conditions that may occur after publication.

📚 Sources

- Apartments.com Multifamily Rent Growth Report – October 2025

- CoStar: Steepest October Rent Decline in 15 Years

- Apartments.com Rent Market Trends

- Zumper Miami Rental Report 2025

- RealPage 2026 Market Forecast

- Yardi Matrix Multifamily Supply Forecast

- BusinessWire – CoStar Multifamily Forecast Update

- Realtor.com September 2025 Rent Research

- Zillow Rental Affordability Report

- NAHB Multifamily Construction Trends 2025

(Additional references available upon request)

{kind=link}